The leftover structure coming from rapid Urban redevelopment in Hong Kong

In the urban development , the land was delineated by “Block” and was subsequently craved or partitioned in a different section and eventually further craved into different sub-section. It resulted a lot of common boundary to each piece of lands adjoining to each other.

The common boundary bought in the typical implication of “party wall” and “common staircase”. There was a blog written by GBE about “party wall”. The reader is welcome to comment. “Common staircase” is what this article goes deep.

The main staircase of the building became as “common” because it was commonly shared between two pieces of land. The common staircase was jointly owned for the enjoyment of the entire building. Since it was common to two adjoining pieces of land, it naturally positioned at the boundary line. It was not a must but naturally came up in the middle between two lots.

Redevelopment and remaining common staircase

With the re-development took place in one piece of land, the adjoining land where the original main building sitting on was necessitated to maintain the common staircase for access. This came up the situation alike to the “Party wall” where the common staircase needs to be retained and still occupy land and space on the land going to be redeveloped.

The first and immediate concern is obviously the common staircase is an enclosed space and fall into the definition of GFA. Nevertheless, this common staircase is nothing helpful and undesirable to new development. To cope with this, the above-extracted part plan has illustrated the example of how the PNAP ADM -2 resolves the GFA problem. In short , the entire footprint of the common staircase be deductible from the GFA calculation. According to PNAP ADM-2 from the Buildings Department, the existing common staircase for an old building can be excluded from site coverage and plot ratio calculation.

Case Study in two adjoining Urban buildings

Building “A” was redeveloped in 1992. The landlord was obligated to leave the common staircase un-touched and exempted its footprint from accountable GFA. Building “B” was subsequently redeveloped in 2008, but the redevelopment of Building B has demolished partly the “common staircase” sitting on the respective piece of land.

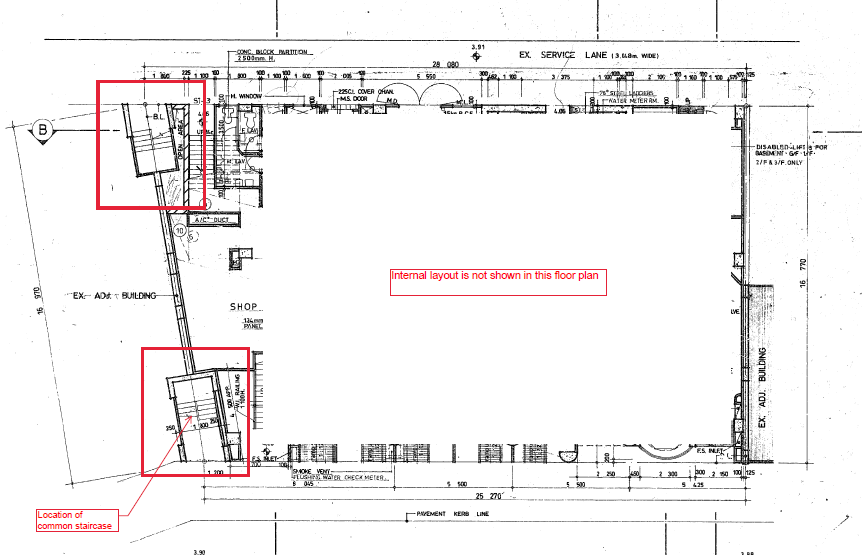

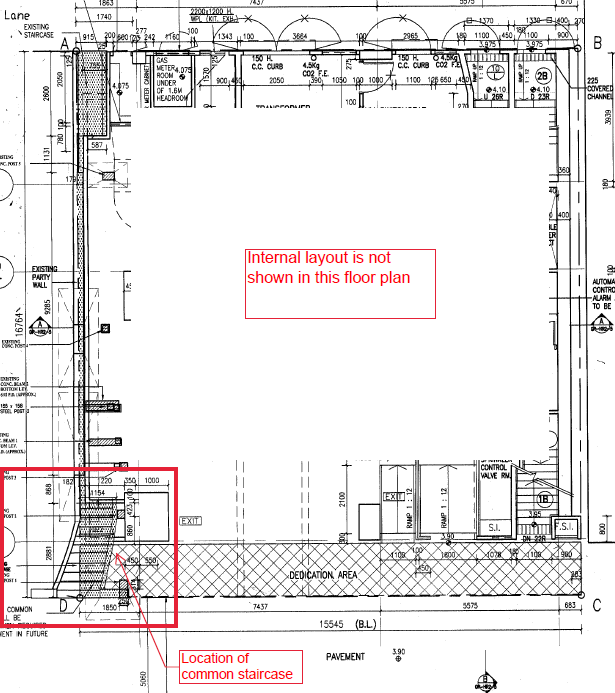

Ground Floor Plan of Building A (showing the Location of Common staircase with Building B)

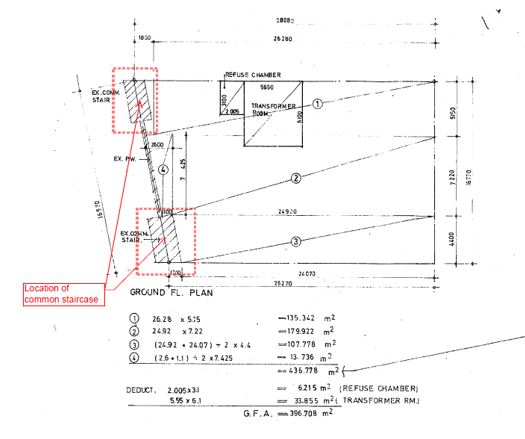

GFA Calculation of Building A

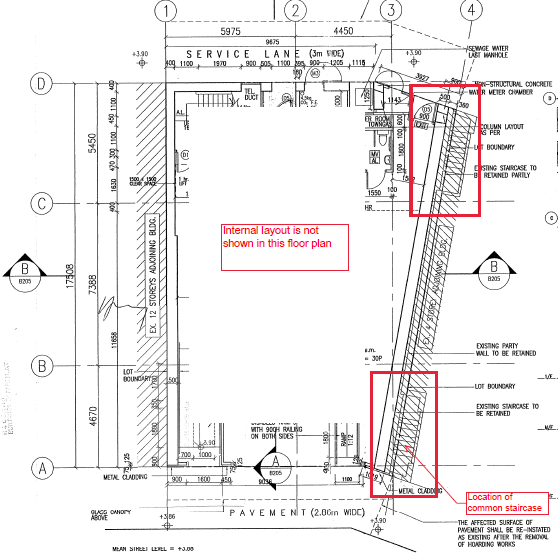

Ground Floor Plan of Building B (showing the Location of Common staircase with Building A)

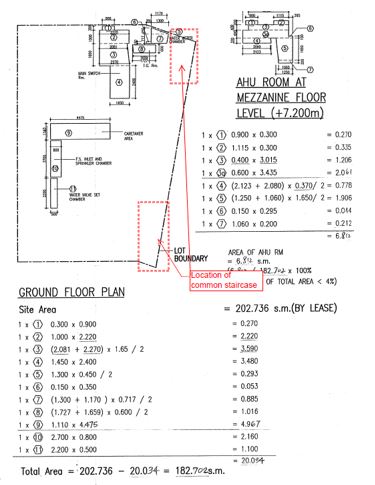

Site Area Calculation in Building B

Another example showing the common staircase issue

Building “C” was redeveloped in 2004, while Building D was redeveloped in 1994. Building “C” and Building “D” retained the common staircase after both redevelopments.

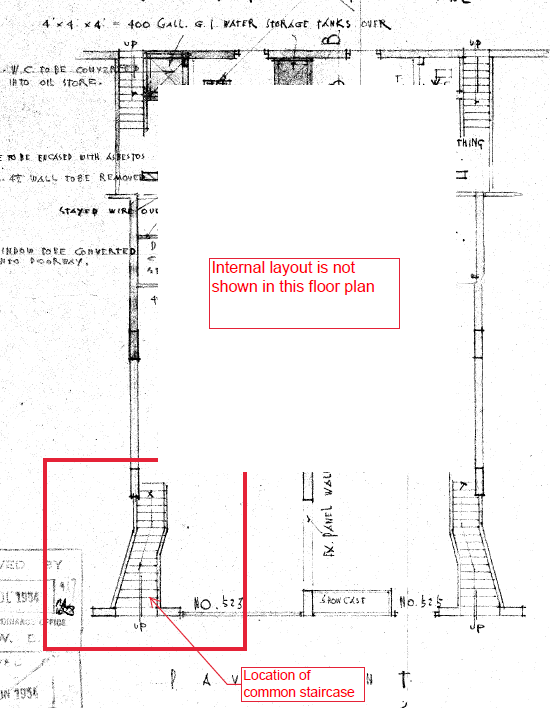

Ground Floor Plan of “Building C”

Ground Floor Plan of “Building D”

Funny interesting maintenance issue

The interesting things come up is that building A which developed earlier than Building B was containing the old “common staircase” . This old left-over common staircase in Building “A” was not GFA counted by the time of redevelopment. The owner of Building A is caught in dilemma. The site where building A sitting on has fully exploited its GFA potential by the time of its redevelopment in 1992. It is now found no surplus GFA be able to assign to this leftover physical ” common staircase” space in the hope to light up again the space utilisation, particularly valuable in highly urbanised city area. The landlord of building A is naturally no incentive to maintain nor convert this common staircase to other proper usage. The only value is the external wall of the left-over common staircase which was being poised for signage in Building “A” (as shown on the photo below. Obviously, the author is wondering the maintenance liability to the grandfather jointly owned structure , i.e Common staircase